IRIS GST TIMES

September ,2019

Issue 1

Chief Editor

Vaishali Dedhia

On this auspicious and pious occasion, we pray to Lord Rama to bless you with Honor, Peace, and Success.

Happy Dusshera!

In this issue, read about key highlights of the 37th GST council covering new GST rate revisions, Optional Annual Returns,and simplified GSTR updates; The issues also covers updates on E-invoicing – the future of GST compliance in India and Provisional ITC under GST.

The feature of the issue is IRIS Sapphire – Enhanced Navigation

The feature of the issue is IRIS Sapphire –GSTR 1 and EWB reconciliation.

Regards,

Team IRIS GST

Export – Import schemes under GST

Government announces RoDTEP – the new scheme worth Rs. 50000 crores to boost exports from India.

As per the Foreign Trade Policy of India 2015-20, 2 schemes were introduces as a part of Exports from India Scheme

- SEIS: SEIS or Service Export from India Scheme is reward-based initiative from the government, wherein a service provider of the notified services, located in India, can claim additional benefits (Duty Credit Scrip) for their transaction on an international market, while still enjoying the perks as provided under GST regime.

- MEIS: Similar to SEIS, MEIS stands for Merchandise Export from India Scheme, awarding exporters of the notified goods with Duly scrips. However,

The government on September 14 announced a new scheme – Remission of Duties or Taxes on Export Product (RoDTEP) – that will replace the existing Merchandise Exports from India Scheme (MEIS) in order to boost exports. However, MEIS shall remain functional until 31st December 2019.

The government also announced that a fully electronic refund scheme on input tax for exporters would be in place by the end of September.

No E-way shall be required for intra-state movement of Goods within Jammu and Kashmir

The Commissioner of State Tax, Jammu and Kashmir vide Notification No. 62 dated September 25, 2019 has notified that no E-way bill shall be required for Intra-state movement of goods within the state of Jammu and Kashmir.

The E-way bill exemption shall be applicable irrespective of the type of goods and value of the goods involved in the movement which commences and terminates within the state of Jammu and Kashmir.

However, the person-in-charge of conveyance must carry documents such as tax invoice, delivery challan, bill of supply or bill of entry, as the case may be.

This notification shall remain effective till October 20, 2019.

IRIS Topaz offers you a 360° solution for all your E-way Bill Needs. A cloud-based tool, IRIS Topaz, provides you with the ability to manage all your tasks related to E-way Bill in an easy and automated way, on the go.

Upcoming Due Dates

GSTR 7 – 10th Oct

GSTR 8 – 10th Oct

GSTR 1 – 11th Oct

GSTR 6 – 13th Oct

GSTR 3B – 20th Oct

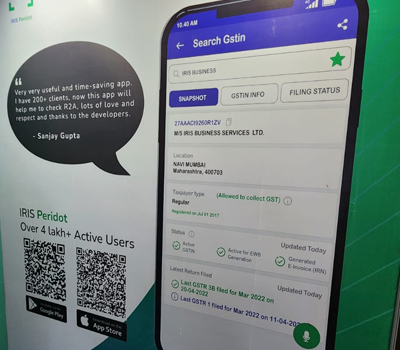

IRIS Peridot against Tax Evasion

- Download Peridot app

- Scan the GSTIN provided on the Invoice

- Check the Compliance status.

- Report any Non-Compliance

You can download IRIS Peridot from

CONTACT US

Have feedback for us?

Want to request for our product demos? Please reach out to us at

+91 22 6723 1000

support@irisgst.com

@IRISGST

37th GST Council Meeting – Key Highlights

The 37th GST Council meeting was held on September 20, 2019, under the chairmanship of Union Finance Minister of India, Smt. Nirmala Sitharaman in Goa. The council meeting concluded bearing good news for all the taxpayers.

The highlights of the 37th GST Council Meeting are as follows:

Optional Annual Returns

As per the 37th GST Council, Annual Return GSTR 9 (for FY 2017-18 And FY 2018-19) has been made optional for taxpayers with an annual turnover below Rs 2 crores. Similarly, Annual Return for Composite Dealers (GSTR 9A) has been completely waived off for the given fiscal years. However, taxpayers with an annual turnover Rs 2 Crore and above will still be required to file their annual returns, along with GST Audit in form GSTR 9C.

A committee of officers shall be constituted to examine and simplify annual GST return form. Furthermore, in order to increase compliance of filing of GSTR 1 (outward supplies) a proposed restriction shall be applicable on availing ITC by entities who do not file GSTR 1.

Simplified GST Returns

The New GST Return filing system under simplified GST regime was supposed to be implemented in a phase based manner from October 2019, will now be introduced with the upcoming FY i.e. from April 2020. Thus, taxpayers will be required to continue filing their GSTR 1 and GSTR 3B until March 2020.

GST Rate Revision

The GST Council has revised GST rates for the following goods and services:

- Plates and cups made of flowers, leaves and bark: Nil

- Caffeinated Beverages: 28%+12% cess

- Supplies to Railways: 12%

- Outdoor Catering (without ITC): 5%

- Woven/ Non-woven polyethylene bags: 12%

- Job work for Diamonds: 1.5

- Supply of Machine Job: 12%

- Marine fuel: 5%

- Almond Milk: 18%

- Slide Fasteners: 12%

- Wet Grinders (Stone as Grinder): 5%

- Dried Tamarind: Nil

- Semi-Precious stones (Cut and Polished): 0.25%

To read our coverage on the previous Council Meet decisions, you may refer here:

E-Invoicing

E-invoicing – a Promising Reality

With the final nod from GST Council, electronic invoicing or e-invoicing under GST shall soon be a reality. A transformational move by the CBIC, e-invoicing can help curb tax evasion drastically and also bring efficiency and ease in GST compliance. Not only this but with e-invoicing, India can join the bandwagon of countries worldwide who have adopted universally accepted standards to streamline their invoicing, taxation and compliance reporting to the Government.

Is E-Invoicing Compulsory In India?

This new invoicing system is expected to be rolled out on a voluntary basis from January 2020 onwards. More information on the implementation model and final formats are anticipated to be released in the coming weeks.

Who Defines The E-Invoice Framework?

After the go-ahead for e-invoicing mandate in India, GSTN along with the Institute of Chartered Accountants of India (ICAI) had published an e-invoicing draft for public consultation. The feedback thus received from the stakeholders, industry associations, businesses and technology enablers shall be incorporated to define the e-invoicing framework for India.

What Are The Benefits Of E-Invoicing System For A Business?

Inter-operability and seamless exchange of data are often the compelling reasons when it comes to implementing standards, not only to the Government but also to the businesses.

At the outset, it may appear to be an additional process that businesses need to follow and efforts will be needed to get data ready as per the specified e-invoice standard. However, with e-invoicing becoming an integral business process,

it will have more benefits to offer, such as:

- Standardization:

- Seamless Reconciliation

- Automation

- Lesser Compliance

- Information Availability

On the other hand, the e-invoicing system will allow the tax authorities to keep a check on under-reporting and reporting of fictitious transactions, which can result in tax evasion.

Which E-Invoice Standard Will Be Followed In India?

The standard for India is currently being formulated. Recently the e-invoice format and the specifications of the data fields in this format was released for public consultation

There exist various standards for e-invoice that cater to varied needs to countries and implementation agencies, there are various standards for an e-invoice. However, looking at the globally used standards, PEPPOL and UBL are indicative of preferable choices.

When GST was introduced in 2017, there was no standard format prescribed for invoices. Until now, the information specified under GST law and rules defined the general framework of invoices under GST. With e-invoice, a standard e-invoice format is expected.

With the implementation of these e-invoices, one can ensure:

- Inter-operability of E-invoices across the entire GST eco-system.

- Uniform machine readability and interpretation of invoice data

- Obviation of data entry errors in the absence of Standard language amongst various players in a business eco-system.

FEATURE HIGHLIGHT

IRIS Sapphire: Navigation Upgrade

With an aim to simplify navigation, the following updates have been made in IRIS Sapphire’s Reconciliation Results:

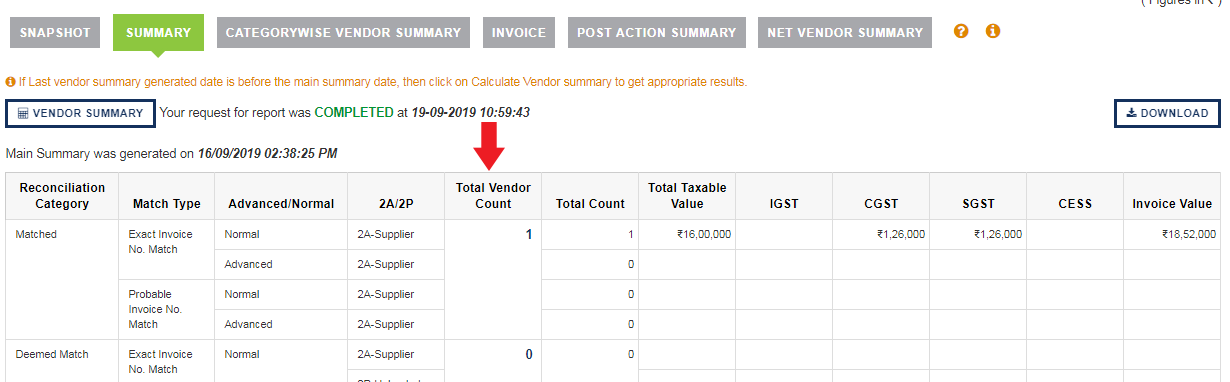

Summary: A new column ‘Total Vendor Count’ has been added for each reconciliation category, wherein the user will be able to see the number of vendors accountable to the total invoice count. For example, if the Matched category has total invoice count of 50 (correlating to 10 vendors), the Total vendor count shall indicate 10 against the 50 matched invoices.

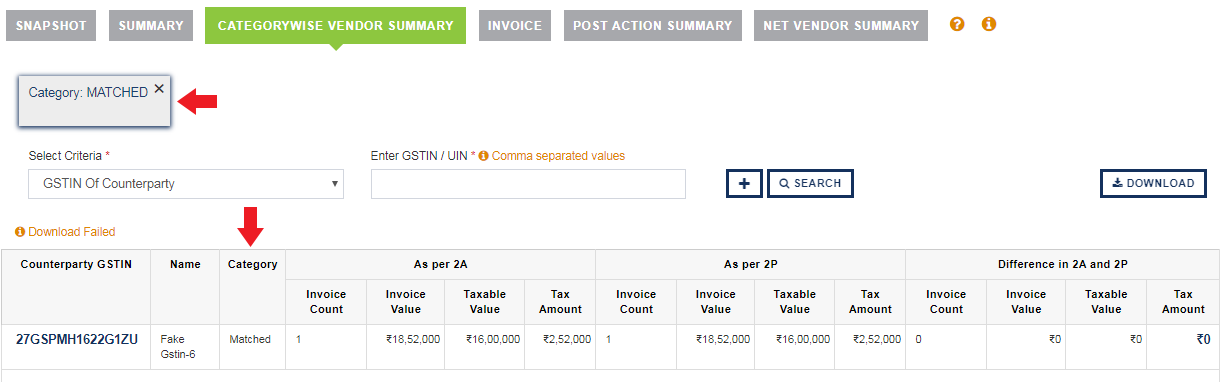

Now, when the user clicks on value under “Total Vendor Count”, he will be navigated to ‘Category-wise Vendor Summary’ tab, wherein he can get a counterparty level summary for the selected reconciliation category.

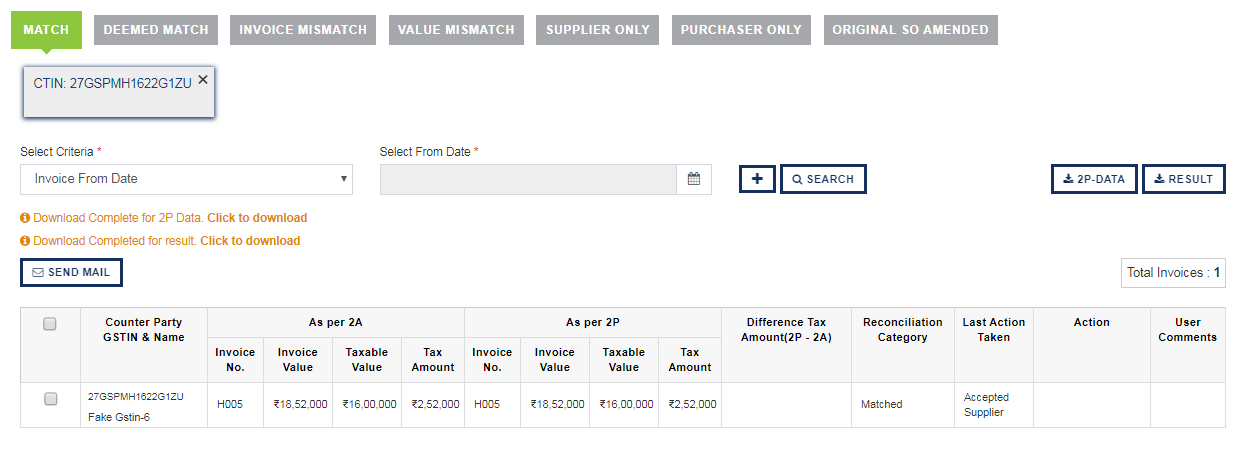

Furthermore, if the user clicks on GSTIN of the vendor from ‘Category wise Vendor Summary’, he will be navigated to ‘Invoice’ tab, whence he shall be able to see detailed list of invoices for that vendor under that reconciliation category.

CDN & CDNA section: the calculation of values has been changed. The new value shall be debit note minus credit note, thereby providing the user with a net tax impact.

Category-wise Vendor Summary: A pre netting to credit debit notes summary, wherein the user will have the option to filter the summary vendor-wise or reconciliation category-wise or both.

IRIS Sapphire is an application built with a highly scalable, available and secure architecture that will help you to file with GST. With built-in analytics and dashboards, IRIS Sapphire will ensure that you stay compliant, while always having a pulse on the process. Click here for free demo

Provisional Input Tax Credit

Provisional ITC

Can I Claim ITC On Provisional Basis Once The New Returns Come In Force?

ITC can be taken if following three conditions are satisfied:

- Purchaser holds the tax invoice of goods/services consumed by him/her.

- Purchaser actually consumes the goods/services purchased by him/her.

- Purchaser makes payment to supplier.

In new returns, once the supplier will upload an invoice in ANX-1, it will be visible to the purchaser in his ANX-2 and he can accept the invoice thereby locking his ITC. This accepted invoice will form part of available ITC in RET-1

Provisional ITC On Missing Invoices

In New Returns Table 4A.10 Provisional input tax credit on documents not uploaded by the suppliers [net of ineligible credit] gives the provision to the purchaser to take ITC on provisional basis. Thus invoices on which purchaser is eligible to take credit but supplier did not upload the invoice can be considered for claiming provisional ITC in the said table.

What Is The Capping To Provisional ITC?

Section 43A of CGST Act states credit available in case of provisional ITC would not be more than 20% of ITC available to the recipient. This available credit is based on the basis of details uploaded by the supplier. Thus, the upper limit stipulated under Section 43A for availing ITC on a provisional basis is 20%. This section would replace the provisions of Section 16(2), Section 37 and Section 38 of the CGST Act which deals respectively with the conditions to avail ITC, details of outward supplies, and details of inward supplies.

Treatment Of Invoices If Supplier Uploads The Missing Invoices In Subsequent Months

Now when provisional ITC is taken by the recipient in one month and in subsequent months, if the supplier uploads the invoice on which provisional ITC is taken, then purchaser will accept that invoice in his ANX-2. By accepting the invoice in ANX-2, it will be auto computed as available ITC in RET-1. However such credit needs to be reversed by the purchaser in table 4B(3) of the main return (FORM GST RET-1) as this credit was already availed provisionally earlier and cannot be availed twice.

Treatment Of Invoices If Supplier Fails To Upload The Missing Invoices In Subsequent Months

The government is taking a risk to the extent of the provisional ITC declared. However they have also taken some precautions by giving a timeline i.e. In case supplier does not upload such invoice till next two filing periods for monthly filers and one filing periods for quarterly filers, then purchaser can upload such invoice as missing invoices in ANX-1 Table 3L.

Table 3L is just an additional reporting of missing invoices by purchasers which will not have any impact on RET-1 being filed.

Thus, though there is a provision made for buyers to claim ITC provisionally, it is advisable to do it with adequate precaution and ensure that the suppliers with whom you are dealing with are compliant. As there is two month of time given to supplier, it is also important to have a proper communication with your suppliers so as to ensure a smooth flow of your ITC.

GST Basics by IRIS GST

Disclaimer: IRIS Business Services has taken due care and caution in compilation of data. Information has been obtained by IRIS from sources which it considers reliable. However, IRIS does not guarantee the accuracy, adequacy or completeness of any information and is not responsible for any errors or omissions or for the results obtained from the use of such information. IRIS especially states that it has no financial liability whatsoever to any user on account of the use of information provided.

{kind=link}

Leave a comment